Fraud Has Moved Beyond the Order

Shopify merchants are seeing the next wave of ecommerce fraud show up before checkout, after delivery, and inside the workflows traditional fraud tools were not built to protect.

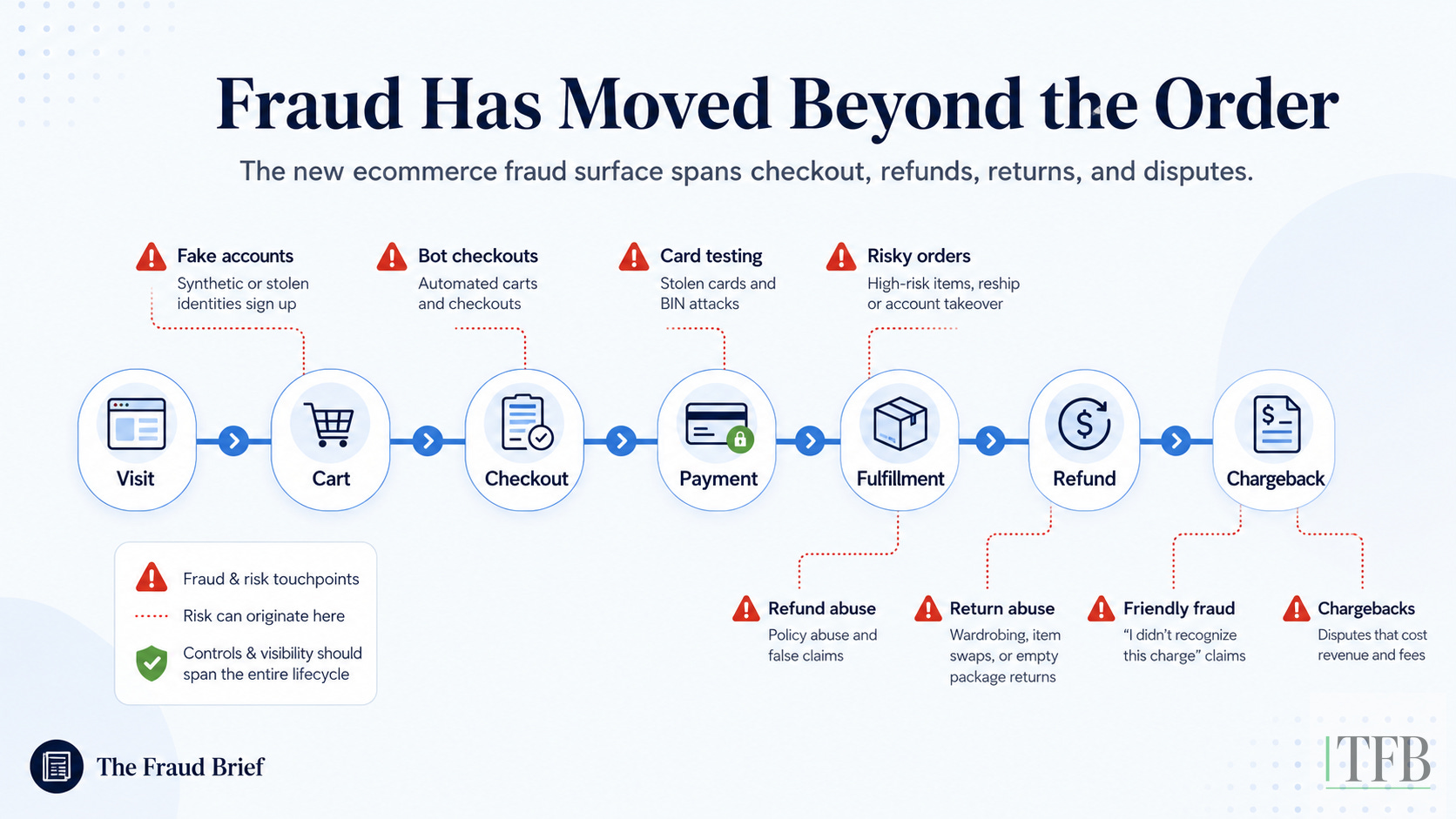

The fraud merchants are dealing with today often starts before an order exists. It shows up as fake abandoned checkouts, failed payment attempts, card-testing bots, fake customer accounts, polluted analytics, damaged email flows, refund abuse, and chargebacks that arrive long after the package has shipped.

In other words, fraud has moved beyond the order.

That shift matters because many ecommerce fraud tools were built around a single moment: the transaction. A customer places an order, a system scores the risk, and the merchant decides whether to approve, review, cancel, or fulfill.

But modern fraud is increasingly attacking the full commerce workflow.

It is not just the payment. It is the checkout path. It is the abandoned cart flow. It is the email system. It is the return policy. It is the refund process. It is the dispute evidence. It is the repeated behavior that only becomes obvious when you connect the dots across time.

That is the new fraud surface.

The old model was order-centric

Traditional ecommerce fraud prevention was built around the order.

A customer checks out. The fraud system looks at signals like billing address, shipping address, IP address, order value, velocity, payment method, and prior chargeback history. Then the merchant receives a recommendation.

Approve.

Review.

Decline.

That model still has value. Merchants still need to identify risky orders before they ship. They still need to avoid chargebacks. They still need to protect revenue and reduce manual review.

But the order-centric model assumes there is an order to evaluate.

That assumption is becoming a problem.

A growing portion of merchant pain now happens before a legitimate order exists. Fraudsters are not always trying to buy the product. Sometimes they are using the store as infrastructure.

They may be testing stolen cards. They may be creating fake customer accounts. They may be generating abandoned checkouts. They may be probing payment flows. They may be rotating names, emails, addresses, and IPs to see what gets through.

The merchant is left with the mess.

No sale.

No real customer.

No clean data.

Just failed payments, fake carts, bad analytics, support confusion, and a store that now has to separate real buyer activity from automated abuse.

The new fraud surface starts before the order

One of the clearest patterns merchants are discussing today is checkout abuse.

A store sees a sudden wave of abandoned checkouts. The names look fake. The emails bounce. The payment attempts fail. The addresses repeat with small changes. The behavior does not look like normal shopping.

That is often not a marketing problem. It is not a conversion problem. It is not necessarily a product problem.

It can be card testing.

In a card-testing attack, fraudsters use automated scripts to test stolen card numbers against checkout pages. They are not interested in the merchant’s products. They are interested in whether the card authorizes.

That distinction is important.

If the attacker is using checkout as a testing endpoint, then product-page behavior may not tell the full story. Storefront traffic tools may miss part of the activity. Traditional order review may come too late because many of the attempts never become successful orders.

But the damage still happens.

Abandoned checkout data becomes unreliable.

Email recovery flows get triggered for fake customers.

Marketing analytics become harder to trust.

Payment attempts create noise.

Staff waste time investigating activity that was never a real buyer.

Good customers can become harder to see because the signal is buried under bot behavior.

This is why merchants are frustrated. They are not only asking, “How do I stop a fraudulent order?”

They are asking, “How do I stop my store from being used this way in the first place?”

That is a very different problem.

The damage is not only chargebacks

Chargebacks are still painful. They are direct, measurable, and easy to understand.

The merchant loses the sale. The product may already be gone. Shipping may be gone. Fees may apply. The dispute process takes time. The bank may side with the customer even when the merchant believes the evidence is strong.

But modern ecommerce fraud creates damage before the chargeback ever appears.

It damages the operating system of the store.

If bots create thousands of abandoned checkouts, the merchant’s abandoned cart metrics become less useful. If fake emails enter recovery flows, sender reputation can suffer. If fraudulent customers create accounts, customer data becomes polluted. If fake payment attempts spike, the merchant has to figure out whether the issue is fraud, payment configuration, checkout friction, or something else.

This is why I think the industry needs to stop treating fraud as only a transaction problem.

Fraud is now an operational problem.

It affects analytics.

It affects customer communication.

It affects fulfillment decisions.

It affects refund policies.

It affects dispute handling.

It affects staff time.

It affects how much friction a merchant feels forced to add for everyone else.

When merchants cannot trust the activity moving through their store, every workflow becomes harder.

Fraud continues after the order ships

The other side of the problem happens after checkout.

An order can look acceptable at payment and still become risky later.

The customer may request a refund with suspicious timing. A return may come back damaged, empty, or inconsistent with the claim. A buyer may say the package never arrived even when tracking says it did. A customer may receive a refund and then file a chargeback. A repeat buyer may show a pattern of refund requests, return abuse, delivery claims, or disputes across multiple orders.

This is where fraud prevention often falls short.

A checkout score is a snapshot. It tells the merchant something about the transaction at that moment.

But fraud is not always visible at that moment.

Sometimes the risk appears in the sequence.

The timing.

The repetition.

The mismatch between behavior and claim.

The history across refunds, returns, support tickets, and disputes.

That is why post-purchase fraud is becoming such an important part of the conversation. Refund abuse, return abuse, friendly fraud, and chargebacks are not separate from payment fraud. They are part of the same lifecycle.

If a merchant only evaluates risk at checkout, they may miss the pattern that develops after the order.

AI and automation make this harder

AI did not create fraud. Automation did not create fraud.

But both make fraud easier to scale.

Attackers can generate fake names, rotate emails, script checkout attempts, test cards faster, create more convincing messages, and manipulate evidence with less effort than before.

That changes the economics.

A fraudster does not need every attempt to work. They can run many attempts, learn from failures, and keep adjusting.

Merchants, on the other hand, have to protect conversion. They cannot simply block everything. They cannot add endless friction. They cannot manually review every strange cart, every failed payment, every refund request, and every chargeback.

That imbalance is the real issue.

Modern fraud is becoming faster, cheaper, and more automated.

Merchant response is still too often manual, fragmented, and reactive.

That gap is where the losses happen.

What merchants need now

The next generation of ecommerce fraud prevention needs to move beyond isolated order scoring.

It needs to understand the full commerce lifecycle.

That means looking at signals across:

Checkout behavior

Failed payment attempts

Account creation patterns

Abandoned cart anomalies

Email and identity signals

Shipping and address repetition

Order timing and velocity

Refund behavior

Return patterns

Delivery claims

Chargeback history

Merchant-specific risk policies

The goal is not to block more customers.

The goal is to make better decisions earlier.

Good fraud prevention should help merchants understand what is happening, why it is risky, and what action makes sense. Sometimes the right action is to block. Sometimes it is to hold fulfillment. Sometimes it is to request verification. Sometimes it is to monitor a pattern. Sometimes it is to approve the order and avoid unnecessary friction.

The key is explainability.

Merchants do not just need a score. They need to know what the score means.

They need to know whether the issue is payment risk, identity risk, address repetition, refund behavior, velocity, or a pattern that has appeared across multiple transactions.

A black-box score is not enough when the fraud surface has expanded across the entire store.

The practical question for Shopify merchants

For Shopify merchants, the practical question is no longer only:

Which orders are high risk?

The better question is:

Where is fraud showing up across my store?

Is it happening before checkout?

Is it happening through failed payment attempts?

Is it creating fake abandoned carts?

Is it tied to repeat addresses, repeat customers, or repeat refund behavior?

Is it showing up after fulfillment?

Is it becoming chargebacks?

Is it affecting analytics, email flows, staff time, or payment risk?

That broader view matters because fraud rarely stays in one lane.

A card-testing pattern may start as failed payments and abandoned carts. A refund abuse pattern may later become chargebacks. A repeat address pattern may look harmless order by order, but obvious when viewed across time.

Merchants need tools that can connect those signals.

Not just to stop fraud, but to operate with more confidence.

The modern solution

Shopify merchants need to move from isolated order review to explainable, lifecycle-aware fraud decisioning.

The goal is not to create more friction for good customers.

The goal is to help merchants identify risky patterns earlier, understand why something looks suspicious, and take action before fraud spreads across payments, fulfillment, refunds, returns, disputes, analytics, and customer communication.

For modern merchants, fraud prevention cannot be limited to one transaction at one moment.

It has to follow the behavior.

It has to explain the risk.

It has to support the workflow.

The next wave of ecommerce fraud is not only about stolen cards or suspicious orders. It is about automated checkout abuse, fake accounts, polluted abandoned-cart data, refund abuse, return patterns, delivery claims, friendly fraud, and chargebacks that appear after the merchant has already done the work.

The merchants who understand this shift will be better prepared.

The tools that win in this next era will not simply score orders. They will help merchants see the pattern earlier, explain the risk clearly, and protect the full commerce workflow.

That is where ecommerce fraud prevention needs to go next.

At Alogram, we are focused on helping Shopify merchants move from isolated order review to explainable, lifecycle-aware fraud decisioning. For merchants seeing suspicious checkouts, failed payment attempts, risky orders, chargebacks, refund abuse, or repeat fraud patterns, our Shopify app is built to help identify those patterns earlier and support faster, clearer action.

Learn more about Alogram for Shopify.

Written by d’Artagnan Osborne, Founder of Alogram, where we are building real-time fraud and payment risk decisioning for modern commerce.