What Has to Be True for Agentic Payments to Work

Faster authorization is only part of the story. The real opportunity is programmable trust.

I’ve been thinking a lot about agentic payments lately, not from the perspective of the underlying technology, but from the perspective of how this actually works in daily life.

Most of the conversation around agentic commerce assumes that the future is simply faster money movement. AI agents will shop, compare, reorder, subscribe, cancel, book, negotiate, and pay on our behalf. That part is probably true. Agents will make intent move faster, and in many cases they will reduce the friction between a decision and a payment.

But I think that is only half of the story.

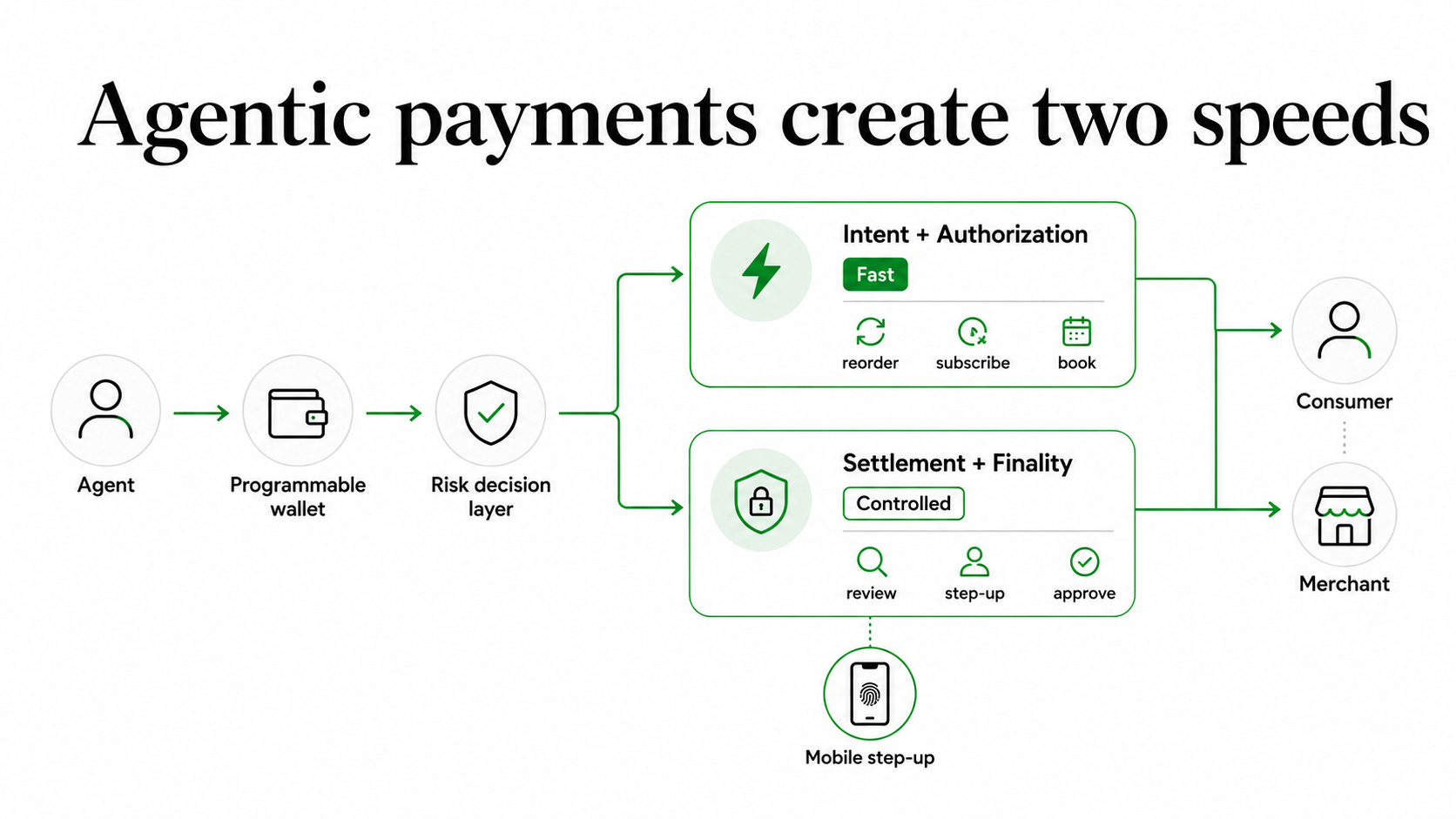

For agentic payments to work safely at scale, the industry will need to accept a somewhat counterintuitive idea: authorization may speed up, but settlement may need to become more controlled.

Once agents are allowed to act on behalf of consumers and businesses, they will need more than a payment credential. They will need a defined operating range. That operating range will likely live in the wallet, or at least be enforced through the wallet, and it will include much more than a dollar limit.

A consumer might allow an agent to reorder household items, renew subscriptions below a certain amount, or book travel only within approved parameters. A business might allow an agent to prepare vendor payments, reconcile invoices, or route payments for approval, but not release funds without a human sign-off.

That is the shift.

The wallet is no longer just a place to store credentials. It becomes a programmable control layer for delegated authority.

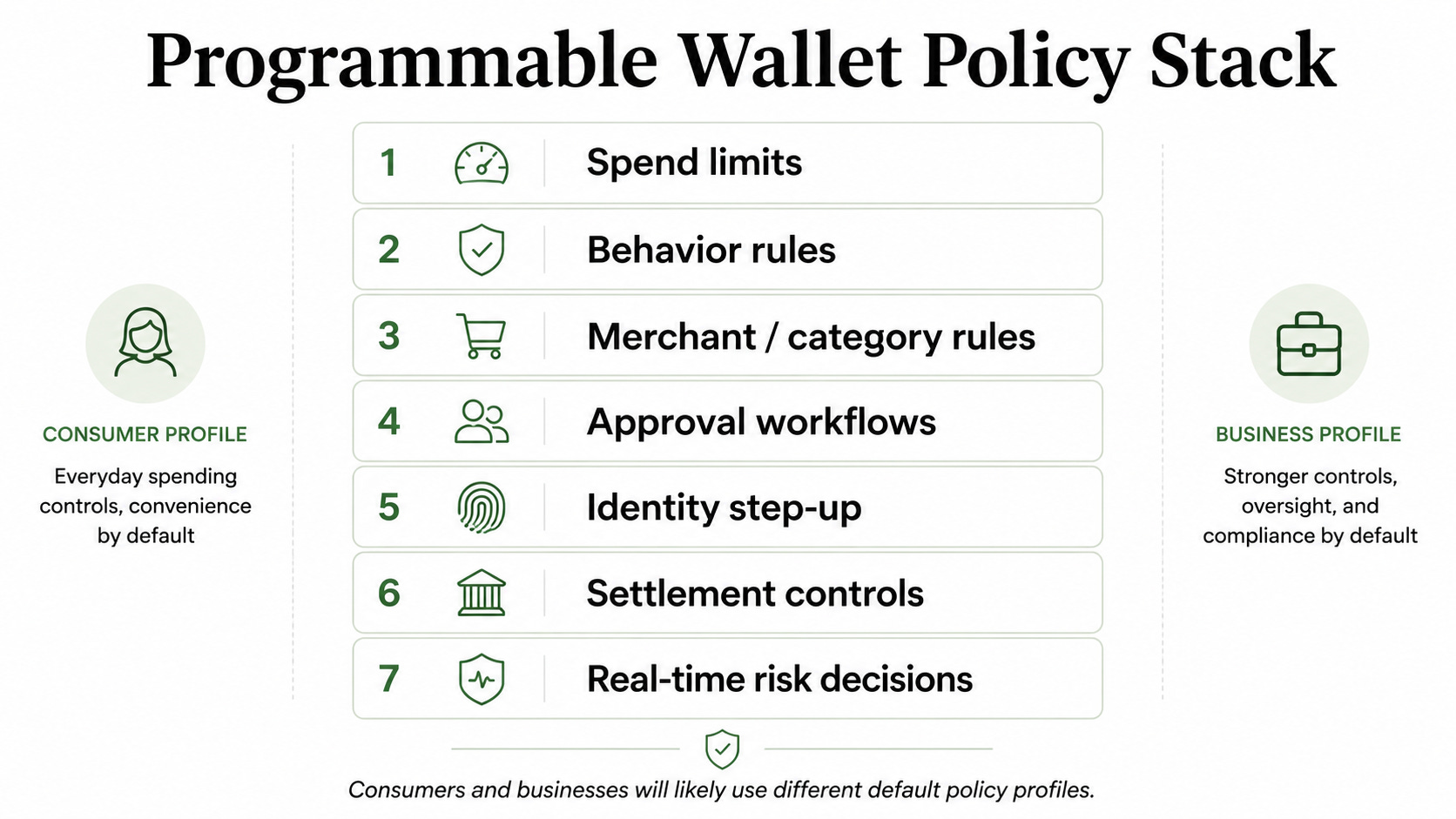

Wallets need to become programmable

When people talk about programmable wallets, the conversation often starts with spend limits. That makes sense, but spend limits are only the beginning.

Agentic payments will require controls around behavior, not just amount.

What merchant categories is the agent allowed to use? How often can it transact? Can it purchase internationally? Can it renew subscriptions? Can it select a new vendor? Can it act without approval during certain hours? Can it authorize a payment but delay settlement? When does it need a stronger identity signal from the user?

These are not edge cases. They are the everyday operating rules that will make agentic payments practical.

Over time, we will likely see default profiles for different use cases. A consumer wallet may have one profile for household purchases, another for subscriptions, another for travel, and another for family spending. A business wallet may have profiles for employee purchasing, vendor payments, recurring invoices, procurement approvals, and treasury-controlled payments.

A consumer agent buying household items should not operate under the same policy as a business agent preparing vendor payments.

The important question becomes less, “Can this agent pay?” and more, “Is this agent acting within the approved policy?”

Authorization and settlement need to separate

This may be one of the most important changes.

In traditional consumer payments, we often think about authorization and settlement as part of one payment motion. A purchase is approved, and the system moves toward finality.

In agentic payments, that may not always be the right model.

Agents will make mistakes. That is not a criticism of agents. It is just part of giving software more responsibility. An agent may misunderstand instructions, optimize for the wrong outcome, choose the wrong merchant, renew the wrong subscription, or complete a purchase before the consumer realizes the implications.

The transaction may be technically authorized, but still not reflect the user’s true intent.

That creates a very different operating environment for fraud, disputes, and risk. Today, “friendly fraud” often implies a consumer disputes a purchase they authorized or benefited from. In an agentic environment, the line becomes more complicated. A consumer may have authorized the agent generally, but not that specific action, merchant, timing, or outcome.

That means the payment system needs more nuance.

Fast intent does not always mean instant settlement. There may need to be reversible windows, risk-based holds, approval workflows, or identity step-up before funds fully move.

The future may be faster authorization, but more controlled settlement.

Business payments will stay more human-in-the-loop

Business payments will evolve differently from consumer payments.

Agents will be very useful in business workflows. They can prepare payments, review invoices, reconcile data, route approvals, flag anomalies, and recommend the next action. In many cases, they will remove a lot of manual work from finance, procurement, and operations teams.

But that does not mean businesses will hand over final payment authority without controls.

For higher-value payments, new vendor relationships, unusual invoice patterns, treasury movement, or regulated workflows, human approval will remain important. The agent may do the work, but a person or defined approval chain may still own the release.

That is not a limitation. It is how trust will be designed into the process.

The practical future of business payments is not fully autonomous money movement everywhere. It is agent-assisted preparation, policy-based routing, and controlled approval.

The phone becomes the practical trust checkpoint

For consumers, the mobile device becomes especially important.

The phone already sits at the intersection of device identity, wallet credentials, biometric unlock, passkeys, location context, and user behavior. That makes it a natural place to perform a stronger trust check when an agent action needs confirmation.

If an agent is acting within a low-risk profile, the transaction may move with very little friction. But if the agent steps outside the expected pattern, chooses a new merchant, crosses a threshold, changes geography, or triggers a risk signal, the phone becomes the moment where the system asks for a stronger proof of intent.

Not every transaction needs more friction.

But some transactions will need a clear way to ask: is this really you, and do you really want this to happen?

That is where device-bound identity, biometrics, wallet approval, and passkeys become practical, not theoretical.

A real-time decision layer becomes necessary

The more agentic payments become part of everyday commerce, the more risk decisions need to happen inside the flow.

Static rules will not be enough. One-time authorization will not be enough. A basic fraud score at checkout will not be enough.

Every agent action may need to be evaluated against permission, policy, identity, behavior, merchant risk, transaction context, approval status, and settlement risk.

This is where I think the real infrastructure opportunity sits.

Not in making every payment faster, but in deciding which payments should move quickly, which should pause, which should require approval, and which should require stronger proof of intent.

At Alogram, this is how we think about the next layer of payment risk. Agentic payments will need a real-time risk and decision layer that can evaluate not only whether a payment is fraudulent, but whether the agent is acting within the right policy and whether the transaction should move, pause, or step up for approval.

That is a different problem than traditional payment fraud.

It is a trust and decisioning problem.

The real shift is programmable trust

Agentic payments are coming, but they will not work simply because agents can initiate payments.

They will work when consumers and businesses can define the boundaries of delegated authority, when wallets can enforce those boundaries, when approval workflows are programmable, and when settlement can be controlled based on risk and intent.

The future of payments is not simply faster payments.

It is knowing when money should move fast, when it should pause, and when the system needs a stronger signal of trust.

That is the foundation agentic payments will need before they become part of daily life.

Written by d’Artagnan Osborne, Founder of Alogram, where we are building real-time fraud and payment risk decisioning for modern commerce.